Why Borrowed Money Doesn’t Belong on Your P&L

Behind the Scenes of a Common Bookkeeping Mistake with Real Cash Consequences | 8 minute read

Cash hitting the bank account usually signals good news for a business. A sale came through, a client paid an invoice, or a project wrapped up successfully.

But sometimes cash arrives for a different reason entirely. A lender may fund a loan, or a business owner may draw on a line of credit.

The bank balance rises either way, but the bookkeeping treatment and tax consequences are completely different. When borrowed money is accidentally recorded as income, then profit increases on paper along with the tax due. Let’s walk through how that mistake can happen and how to spot it before it gets expensive.

Borrowed Money Is Not Income

When a business receives a loan, two things happen at the same time.

The business receives cash, and it also takes on an obligation to repay that cash.

In accounting terms, assets and liabilities are both increased by the same amount. The business has access to additional funds, but it is not any richer.

In many bookkeeping systems, including QuickBooks Online, the transaction first appears in the same place every other deposit appears: the bank feed. Without context, a deposit from an unfamiliar source can look exactly like revenue from a new client to a new bookkeeper or an automated system suggesting categories.

Case Study: Receiving a Small Business Loan

Imagine a small consulting business receives approval for a $20,000 working capital loan in January. The lender deposits the funds directly into the business checking account. From the bank’s perspective, this is just another deposit that will flow to the bookkeeping system. But what happens on the books?

Avoiding the Mistake: Receiving Loan Proceeds

If the person reviewing the bank feed knows a loan is coming, the deposit would normally be categorized to a liability account such as Loan Payable.

Once categorized, the bookkeeping system records the following journal entry behind the scenes.

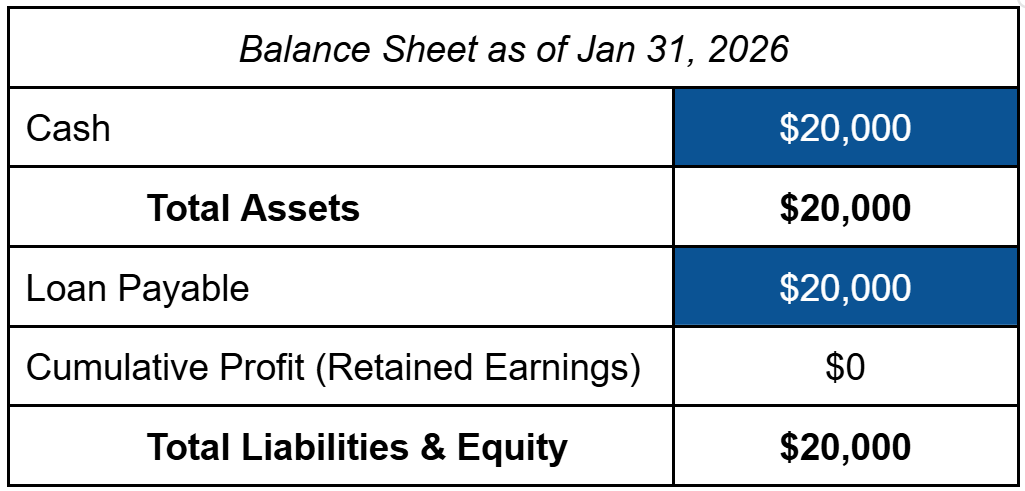

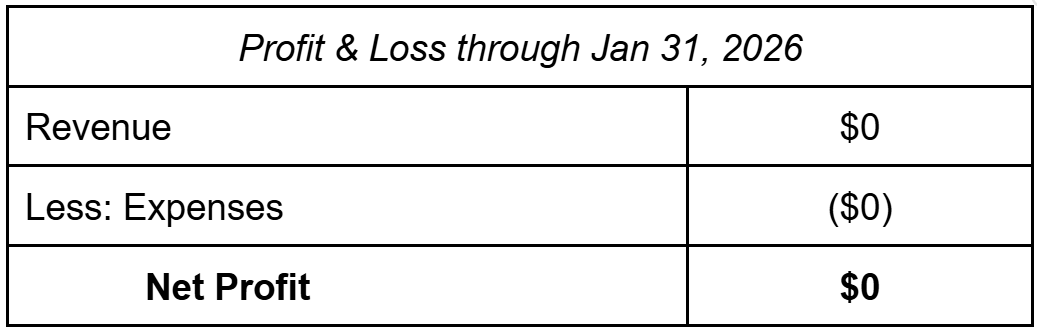

After posting the journal entry, this is how the business’ financial statements would look:

After the entry posts, the financial statements reflect what actually happened. The bank account shows $20,000 of cash, and the balance sheet has a matching $20,000 loan payable liability.

The Profit & Loss statement does not change because no income was earned and no expenses were incurred. The business just received financing that will be paid back over time.

The Classic Mistake: Loan Recorded as Income

Now imagine the same $20,000 deposit appears in the bank feed, but the bookkeeper is not aware of any financing activity. In some cases, there may be no dedicated bookkeeper at all, and staff simply accept the system’s suggested categorizations. A category like “Sales” or “Revenue” may seem like a reasonable choice for a deposit with a vague bank description. In some systems, integrated AI agents may even suggest a revenue account based on past activity. If automatic posting settings are enabled, the transaction may be categorized and recorded without anyone reviewing it. In that case, the system would record the following journal entry.

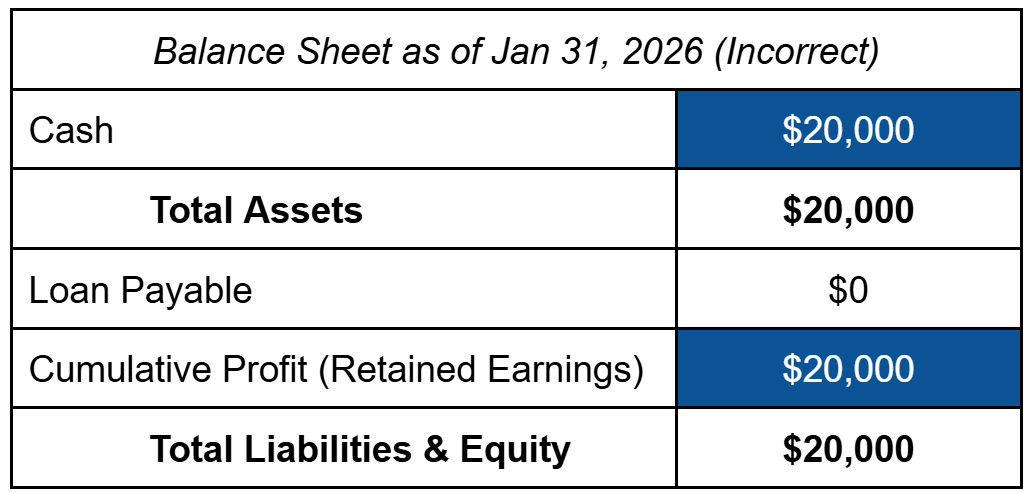

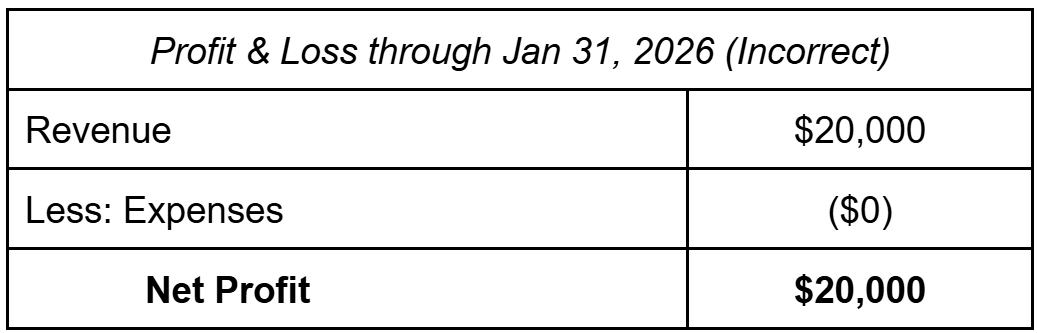

After posting the journal entry, this is how the business’ financial statements would look:

After the entry posts, the financial statements tell a very different story from the first scenario. The bank account still has $20,000 of cash, but the balance sheet no longer reflects the loan payable liability. Instead, the Profit & Loss statement now shows $20,000 of revenue. On paper, it appears the business earned $20,000 of taxable income in January.

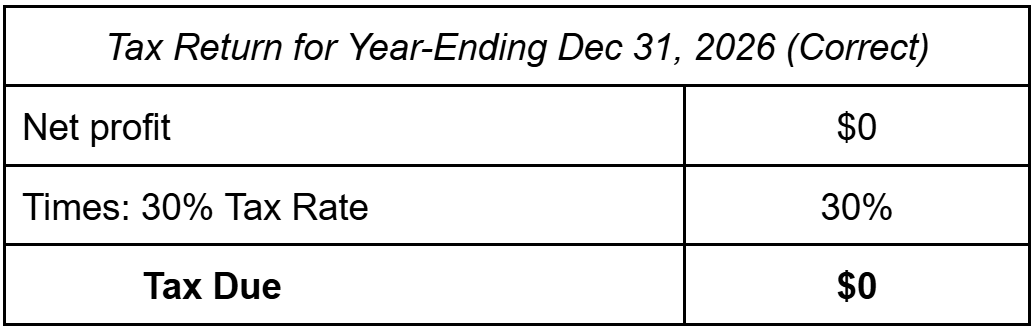

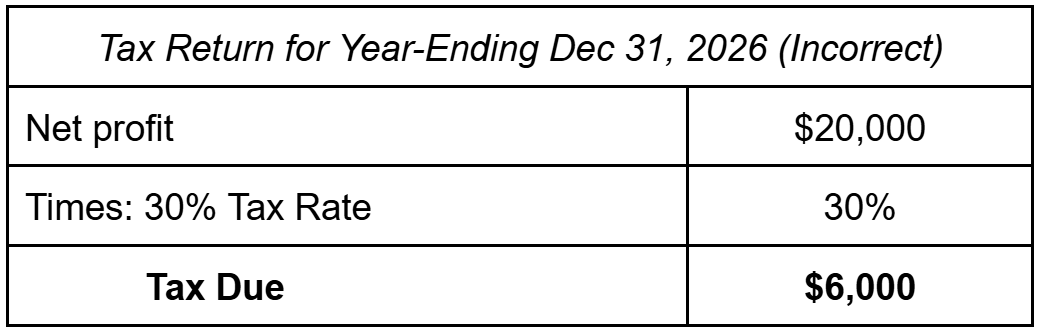

The Tax Consequences

Let’s assume the business owner expects to pay around 30 percent in combined federal and state taxes.

Under the correct treatment, the loan has no tax effect.

Under the incorrect treatment, the books show $20,000 of income that will flow directly into the tax calculation if not corrected.

Bookkeeper’s Note: A quick way to spot this error before it happens is to compare large deposits in the bank feed with the list of issued invoices. If a deposit doesn’t tie to an invoice or sales report, it may represent financing rather than income. Most loan deposits can be confirmed by reviewing the loan agreement, funding confirmation email, or lender statement once you know there’s a loan to look for.

How to Fix the Error

If this error shows up in the books, the correction is usually manageable when caught early.

Start by locating the deposit that was recorded as revenue and reclassify to a fitting liability account like Loan Payable.

Next, review any payments that have already been recorded. Loan payments typically include two components: principal, which reduces the loan balance, and interest, which compensates the lender for their risk.

Split the payments so the principal portion reduces the Loan Payable account, and the interest portion is posted to Interest Expense.

Once the corrections are made, updated Balance Sheet and Profit & Loss reports should show the loan as a liability and remove the phantom income.

If the deposit was recorded as revenue in a year where the tax return has already been filed, the situation may require additional review. A bookkeeper can help determine how much income was created by the misclassification, and the tax preparer who filed the original return can advise on whether any adjustments or amended filings are appropriate.

As with many bookkeeping issues, these fixes are much easier when the mistake is identified early, and always reach out to a qualified tax professional for personalized support and recommendations.

When Loans Do Affect the P&L

Borrowed money itself does not belong on the Profit & Loss statement, but that does not mean loans never affect profit.

The most common way a loan touches the P&L is through interest expense. When interest accrues or is paid, it appears as an expense and reduces profit. For example, if the business pays $500 of interest on the loan before making any principal payments, the transaction would result in the following journal entry:

There is another situation where loans can affect profit, though it happens less often. If a lender forgives part of a debt or settles a loan for less than the amount owed, the forgiven portion can be considered income. For example, if a lender agrees to cancel $5,000 of a remaining loan balance, the books would record:

In that case, the business no longer owes the money, so the balance sheet liability disappears and the P&L reflects a gain that will generally be taxable to the business. Outside of situations like interest or debt forgiveness, borrowed money itself does not change profit.

What about Merchant Cash Advances (MCAs)?

Merchant cash advances (often called MCAs or revenue advances) are another form of financing that can easily be misunderstood in the books. Instead of a traditional loan with fixed monthly payments, these arrangements provide a lump sum of cash today in exchange for a portion of future sales until a predetermined amount has been repaid. They are often advertised as fast, flexible funding for businesses that need cash quickly, with approvals based on recent sales activity rather than traditional credit underwriting.

In a future Nebula Bookkeeping blog post, we will take a closer look at how these arrangements work and the most common bookkeeping issues they cause.

TL;DR

Borrowed money can look just like revenue when it appears in the bank feed. If loan proceeds are categorized as income, then profit increases even though the business has not actually earned anything new. That can lead to unnecessary tax being calculated on money that still needs to be repaid.

Most bookkeeping errors are easy to miss until someone takes a closer look at how the transactions were recorded. If you need help reviewing your books or setting up your systems correctly, Nebula Bookkeeping works with small businesses to keep their financial records aligned with what is actually happening in the business.

Looking for bookkeeping support? Nebula Bookkeeping can help!