The #1 Most Expensive Bookkeeping Mistake

And How to Avoid It (With Pictures) | 9 minute read

For many business owners, bookkeeping can feel like floating through space: If there’s oxygen in the tank, or cash in the bank, and no flashing warning lights, things seem under control. But, in bookkeeping and space walking, any small miscalculations can compound into disasters by the time a drift is visible. Inaccurate books rarely fail in dramatic ways. They tend to leak quietly, and result in expensive course corrections.

One of the most disastrous bookkeeping mistakes is overstating profit. If net profit is overstated, then taxable income and taxes due will be overstated too. And that has a real cash effect! Let’s explore below the most common and the most expensive real-life ways profit overstatement can occur.

The Most Common Mistake: Missing Expenses

The most common way profit gets overstated is surprisingly simple: expenses never make it onto the books.

This usually happens when perfectly legitimate business purchases are made with a personal card or unlinked account either by accident or through a comedy of errors. The expense is real. The cash is spent. But if it is not recorded, the expense (and associated tax deduction) will get lost in the shuffle. The result:

Expenses look lower. Profit looks higher. And higher taxes follow right behind.

Nothing dramatic happens in the moment. There is no flashing error message. Just a slow widening gap between what the business actually earned and what the Profit & Loss (P&L) reports say it earned. Over time, that gap can translate into thousands of dollars of unnecessary tax paid on income that was never truly profit.

But isn’t this something a tax accountant should catch?

Tax preparers see year-end totals and rarely comb through every individual transaction. They may ask questions like “Are these books complete?” or “Did you pay for any other business expenses that aren’t shown here on the books?” But a tax accountant can only include as many deductions as you record or can remember and document. By tax-time, they are generally just checking for reasonableness. So, if the numbers aren’t wildly off, issues can slip through unnoticed.

But there’s another mistake I see constantly that can be even more frustrating.

The Most Expensive Mistake: Double-Counting Income

Income is often doubled up in bookkeeping systems when an invoice is recorded correctly, but then the related bank deposit is recorded incorrectly as new income instead of being matched to that original invoice.

Unlike missing expenses, which inflate profit gradually, double-counted income can spike profit quickly. And unless someone is reviewing the balance sheet with intention, the mistakes can hang around long enough to make their way onto a tax return.

Let’s look at an example of how this might happen. The screenshots in this case study are from QuickBooks Online, but similar issues can arise within any bookkeeping system.

Case Study: Invoicing for Services

Let’s say I performed some bookkeeping services for a happy client and sent them an invoice on December 01, 2025 for $800 which is due to be paid by December 31, 2025.

As a result of creating the invoice, the bookkeeping system posts this back-end journal entry:

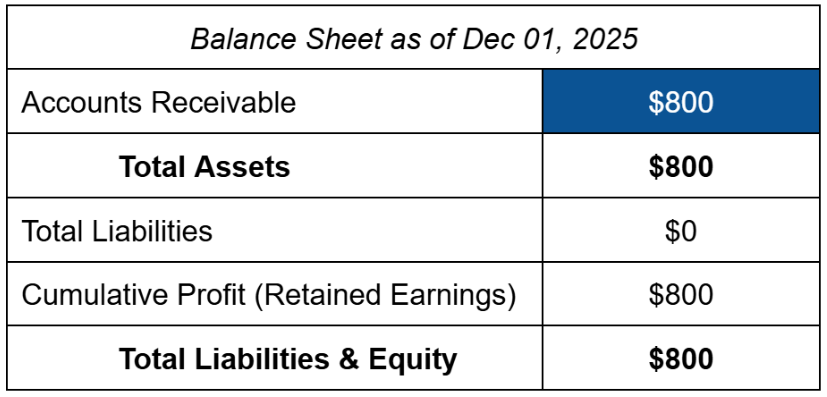

After the journal entry, here are the financial statements as of December 01, 2025:

Perfect. The reports correctly reflect reality on December 01, 2025. I have completed and recognized income for $800 worth of services, and a client is planning to pay me $800.

Later, the $800 payment will hit the bank feed. This is where things could go sideways.

Avoiding the Mistake: Matching Income

My client pays the full amount due and $800 is deposited to my business bank account by December 31, 2025. Here is what that might look like from the bank feed:

The bookkeeping system automatically finds the related invoice, or I can look up the invoice manually. Either way, I select the option to match the bank transaction to the original invoice. The system recognizes that this is cash received as payment for services already rendered and recorded. It will simply reduce the amount owed from the client by the amount just paid.

As a result of matching the bank deposit to the invoice, the bookkeeping system posts this journal entry in the background:

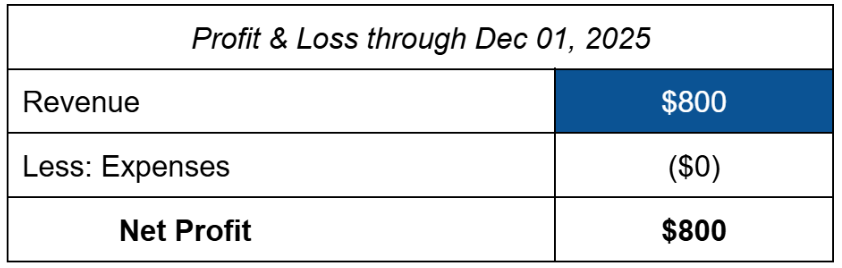

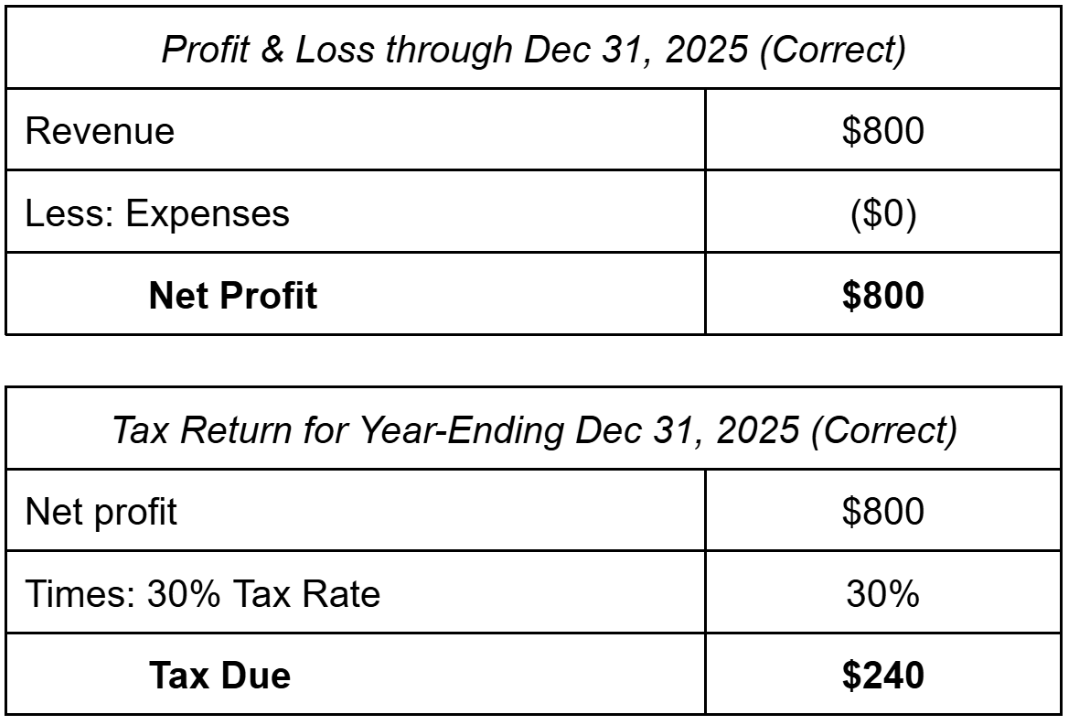

After the journal entry, here are the financial statements as of December 31, 2025 and the related tax calculation:

This treatment still results in financial statements that reflect reality. I performed $800 worth of services and received $800 of cash. My client has paid in full and owes me no additional amounts. After paying $240 of taxes on the $800 of income, I will still have $560 left in the bank account to reinvest into the business.

The Classic Mistake: Creating New Income

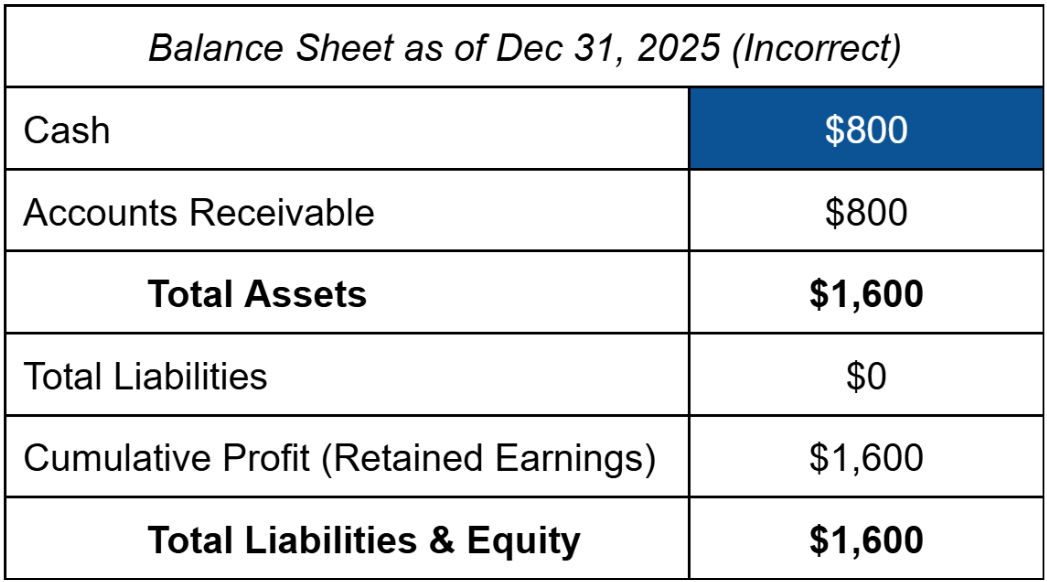

But what would happen if the system didn’t automatically suggest a match to the original invoice and I didn’t know to look for one? Well, I would be tempted to categorize this transaction to a sales or revenue account. But that would be an expensive mistake!

As a result of categorizing the bank deposit as sales revenue, the bookkeeping system posts this journal entry:

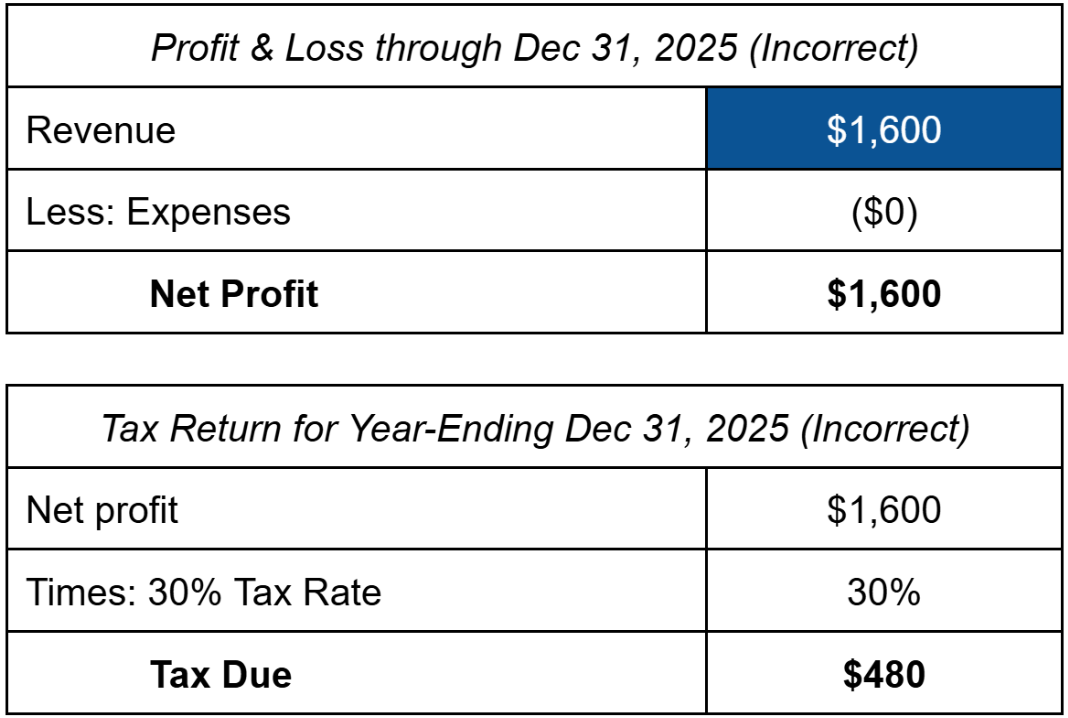

After the journal entry, here are the financial statements as of December 31, 2025 and the related tax calculation:

Something feels off when comparing the financial statements to reality after this mistake. I do have $800 in the bank, so that’s okay. But there’s also an $800 Accounts Receivable asset on the balance sheet. If I went to the client and asked for another $800 for the services they already paid for, I’d be in for a one-star review!

And what about the tax bill? Based on $1,600 of revenue and a presumed tax rate of 30%, my income tax due would be $480. But, in real life I only did $800 of work and collected $800 of cash. That extra $800 of “income” exists only in the bookkeeping system, but the IRS does not know that! After I pay $480 of tax from my $800 bank balance, I will only have $320 left in the account to reinvest in my business. Between the correct and incorrect scenarios, there was the same business activity, the same client, and the same $800 payment. The only difference was I paid twice as much tax!

This is why reviewing the balance sheet matters. If your Accounts Receivable balance does not represent real money you could actually go collect, something is off. Often it is paid invoices still marked as “receivable”, because the payment was recorded incorrectly.

Pro tip: Another easy way to identify this error is to look at activity detail in all the income accounts. An invoice may be set up to post income to one account like “Sales,” while the unmatched deposit is categorized to a similar account like “Sales Revenue.” Because each part of the doubled income is posted to different accounts, it may be missed during standard account reviews. Wherever possible, substantially similar accounts should be consolidated to avoid oversights and confusion.

How to Fix It

So what’s the next step if you find this error in the books? It depends on how much time has passed. If the double counting occurred in the current year or is caught before the tax return is filed. Then the correction is usually straightforward. Here are the steps:

Identify all double-counted deposits in the bank feed.

Undo the deposit categorizations.

Select the suggested invoice to match or manually look up the invoice and select “Match”.

Review the Accounts Receivable or Sales Clearing balance sheet account (wherever the invoices or sales channel payouts initially posted) and confirm that the balances reflect real income you can expect to receive.

Run new Balance Sheet and P&L reports and re-reconcile the bank accounts.

If the error occurred in a year for which the tax return has already been filed, things may be a little more complicated. Here is one potential approach:

Work with a bookkeeper to identify how much income has been double counted in each tax year.

Contact the tax accountant who filed the original returns to discuss potentially filing amended returns, reporting the corrected income amounts, and requesting refunds for overpaid tax.

Choosing whether to file amended tax returns can be a layered decision, so make sure to reach out to a qualified tax professional for support and recommendations. This article is not intended to be tax advice! It is a case study based on common experiences created for informational and educational purposes only.

TL;DR

While the most common bookkeeping mistake is missing out on business expenses, the most expensive is double-counting income by not matching invoices or sales channel payouts to bank deposits. Missing deductions and double-reported income can result in thousands of dollars of additional tax. These mistakes can be fixed, but the process is much easier when they’re caught early!

Looking for bookkeeping support? Nebula Bookkeeping can help!